Analyst Forecast Data Feeds Are Not What They Used To Be

with Henry Laurion, Alastair Lawrence, and Nicholas Martin

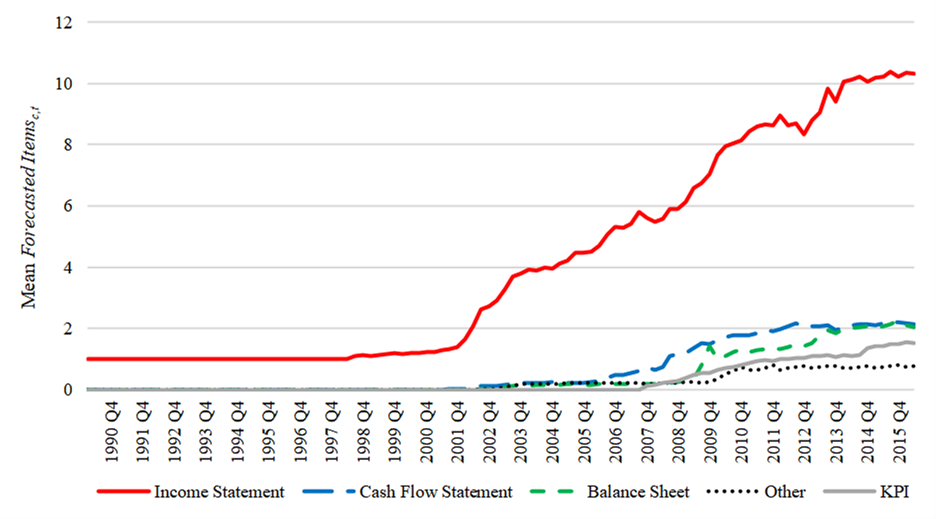

We highlight that since 2001, the number of one-quarter-ahead financial items that are both forecasted by analysts and then disseminated via FactSet and I/B/E/S data feeds has soared from 5 to 170+. We show that the consequent growth in the quantity and richness of income statement, cash flow statement, balance sheet, ratio/other, and KPI forecast surprises is associated with increases in the information content of earnings announcements, and the mapping of news about accounting fundamentals into stock returns. Our study speaks to the economic role that financial data providers play in disseminating analyst forecasts, and the effects that such dissemination has on the informativeness of financial statements.

Biases in Analysts’ Multiyear Forecasted Income Statements, Balance Sheets, and Cash Flow Statements

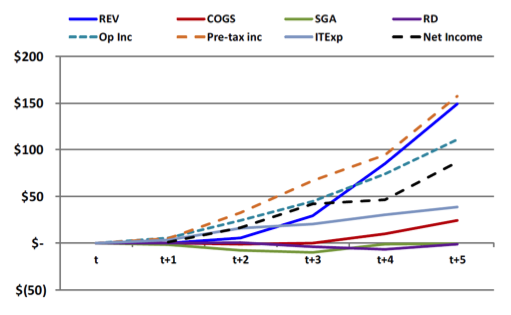

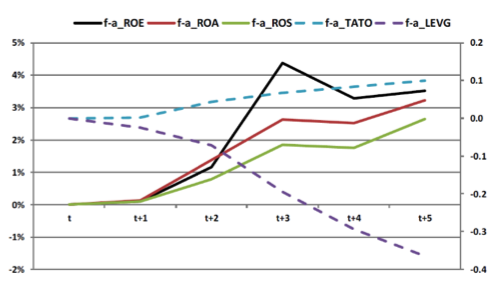

Analysts make optimistic forecasts of long-horizon EPS, ROE, ROA, ROS and asset turnover, driven by overly bullish projections about revenues and all common-sized expenses except income tax, which they forecast pessimistically. Analysts are also optimistic about long-horizon operating cash flows and operating accruals. While they are unbiased in their forecasts of long-horizon total assets, they underestimate long-horizon debt and overestimate long-horizon equity. Our regressions support the view that analysts strategically inflate their long-horizon forecasts of EPS the more intangible and hard-to-verify are firm assets.

Selected Publications (Past 10 Years)

The Characteristics that Provide Independent Information about Average U.S. Monthly Stock Returns

with Jeremiah Green and Frank Zhang.

Forthcoming, Review of Financial Studies.

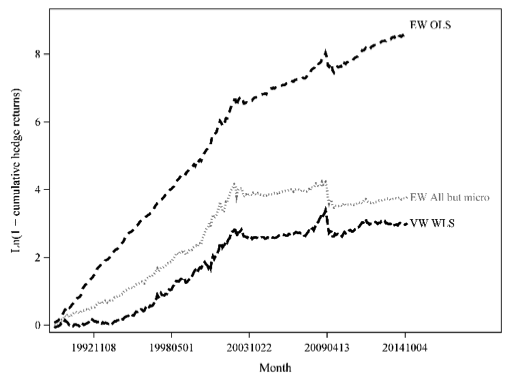

We take up Cochrane’s (2011) challenge to identify the firm characteristics that provide independent information about U.S. monthly stock returns by simultaneously including 94 characteristics in Fama-MacBeth regressions that avoid overweighting microcaps and adjust for data snooping bias. We find that return predictability fell sharply in 2003 such that just two of the 94 tested characteristics have been independent determinants since then. Equivalently, the monthly hedge returns to exploiting characteristics-type predictability have been essentially zero since 2003 in non-microcap U.S. stocks.

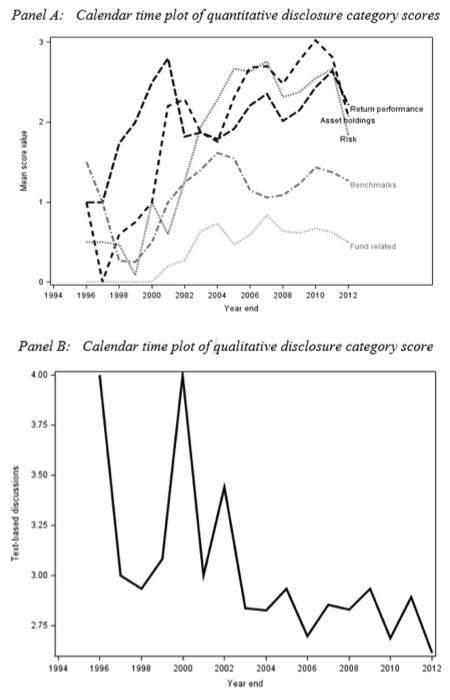

Hedge Fund Voluntary Disclosure

with Jeremiah Green and Frank Zhang.

Forthcoming, The Accounting Review.

We study 3,234 letters sent by 434 hedge funds to their investors in 1995–2011. Contrary to the industry’s reputation for opacity, managers provide their investors with an array of quantitative and qualitative information about returns, risk exposures, holdings, benchmarks, performance attribution, and prospects. We find that the tensions between the agency costs faced by investors and the proprietary costs faced by managers affect fund disclosures. Consistent with managers reducing proprietary costs, better-performing funds disclose less quantitative data about performance and holdings, and consistent with the presence of agency costs, riskier funds disclose less quantitative information about performance and assets under management.

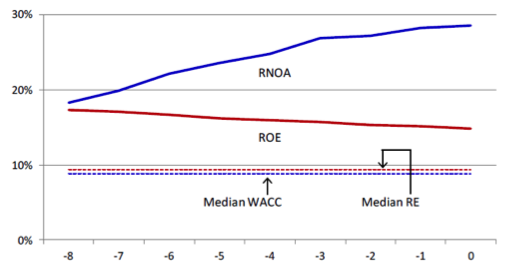

The Dual Use of Residual Income and DCF Valuation Methods by U.S. Sell-Side Equity Analysts

with Joshua Coyne, Jeremiah Green and Frank Zhang.

Forthcoming, Journal of Financial Reporting.

We find that residual income (RI) methods are used just 1/20th as often as DCF by U.S. sell-side equity analysts, and that analysts sometimes arrive at different DCF and RI valuations for the same firm in the same report. We use such dual valuations to gain new insights into the characteristics and performance of RI and DCF. We show that RNOA-RI valuations are optimistic relative to future stock prices and embed forecasted RNOAs that increase toward a terminal year median of 28%, whereas ROE-RI valuations are unbiased as compared to future stock prices and contain ROEs that decline toward a terminal year median of 17%.

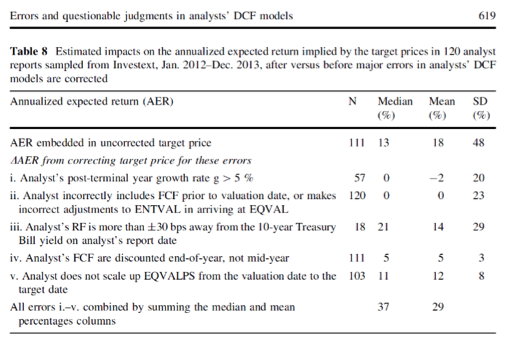

Errors and Questionable Judgments in Analysts’ DCF Models

with Jeremiah Green and Frank Zhang.

Review of Accountings Studies (2016).

For 120 DCF models detailed in reports issued by U.S. brokers in 2012-13, we find that sell-side equity analysts make a median of three theory-related and/or execution errors and four questionable economic judgments per DCF. Recalculating analysts’ DCFs after correcting for major errors changes analysts’ mean valuations and target prices by -2% to +14 % per error. Based on face-to-face interviews with analysts and those who oversee them, we conclude that analysts’ DCF models are semi-sophisticated: analysts make mistakes regarding certain aspects of correctly valuing equity but also respond rationally to the strong incentive that they are not directly compensated for being textbook DCF correct.

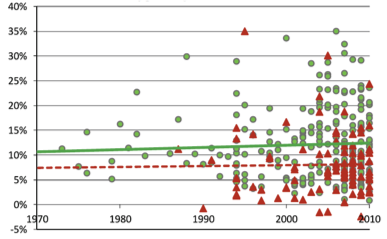

The Supraview of Return Predictive Signals

with Jeremiah Green and Frank Zhang.

Review of Accounting Studies (2013).

This study describes and analyzes the return predictive signals (RPS) publicly identified over the 40-year period 1970–2010. Our supraview brings to light new facts about RPS, including that more than 330 signals have been reported; the properties of newly discovered RPS are stable over time; and RPS with higher mean returns have larger standard deviations of returns and also higher Sharpe ratios. Using a sample of 39 readily programmed RPS, we estimate that the average cross-correlation of RPS returns is close to zero.

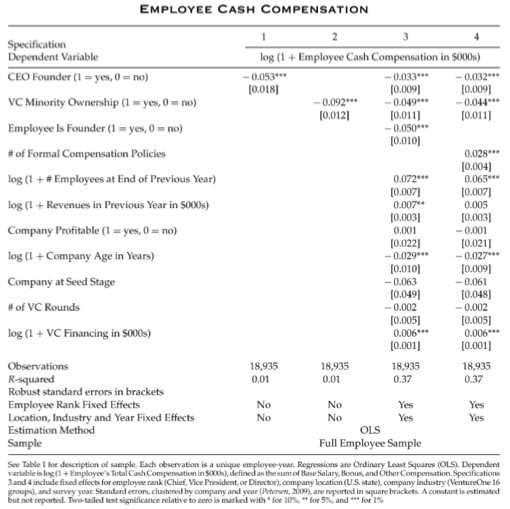

Employee Compensation in Entrepreneurial Companies

with Ola Bengtsson.

Journal of Economics & Management Strategy (2013).

To shed light on the central role played by employee human capital in entrepreneurship, we study 18,935 non-CEO compensation contracts in 1,809 privately held VC-backed companies. Our key finding is that employee compensation varies with the degree to which VCs versus founders control the business. We show that relative to founder-controlled firms, VC-controlled firms pay their hired-on (i.e., nonfounder) employees higher cash salaries, provide stronger cash and equity incentives, and have more formal pay policies in place. We also observe that founder employees earn less cash pay and face weaker cash incentives than do hired-on employees, but have stronger equity incentives.

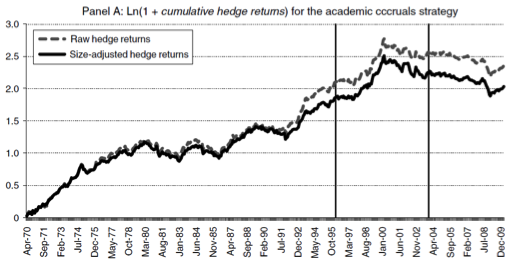

Going, Going, Gone? The Apparent Demise of the Accrual Anomaly

with Jeremiah Green and Mark Soliman.

Management Science (2013).

Consistent with public statements made by sophisticated practitioners, we show that the hedge returns to Sloan’s (TAR, 1996) accruals anomaly appear to have decayed in U.S. stock markets to the point that they are, on average, no longer reliably positive. We explore some potential reasons why this has happened. Our empirical analyses suggest that the anomaly’s demise stems in part from an increase in the amount of capital invested by hedge funds into exploiting it, as measured by hedge fund assets under management and trading volume in extreme accrual firms. A decline in the size of the accrual mispricing signal, as measured by the magnitude of extreme decile accruals and the relative persistence of cash flows and accruals, may also play a (weaker) role.

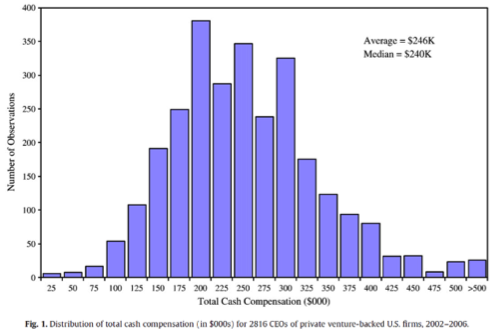

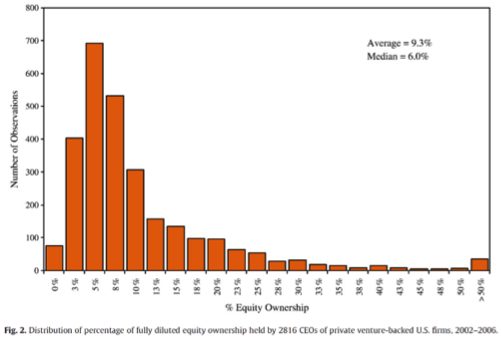

CEO Compensation in VC-backed Firms

with Ola Bengtsson.

Journal of Business Venturing (2011).

We hypothesize that because fast-growing young companies must raise money in private capital markets that contain significant financing frictions, the CEOs of such firms will be compensated for successful fundraising. Using a sample of 1,585 private venture-backed U.S. firms during 2002-2006, we find that the cash pay of entrepreneur-CEOs is increasing in both the quantity and quality of financing secured and is more sensitive to successful fundraising the more challenging and difficult is the fundraising task. Successful fundraising also increases the gap between the pay of CEOs and other executives. Finally, we show that while VC financing dilutes the CEO’s fractional equity ownership, it increases the dollar value of that ownership.

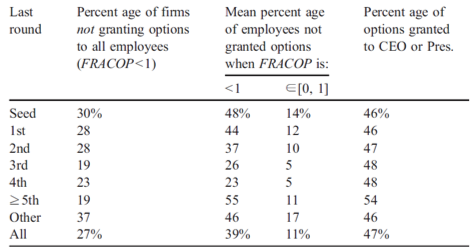

Give Everyone A Prize? Employee Stock Options in Venture-Backed Firms

Journal of Business Venturing (2008).

I examine employee stock options in private entrepreneurial firms. I focus on private U.S. VC- backed firms because they are renowned for the intensity and organizational depth of their stock option grants. Contrary to stereotype, I show that 27% of U.S. venture-backed firms do not grant stock options to all employees. I explain this by theorizing that the economic and legal settings in which venture-backed companies exist lead to both costs and benefits from the use of stock options to attract, compensate, incent, monitor, and retain certain employees, and that sometimes the costs exceed the benefits. I test the theory by determining whether variation in the organizational depth to which venture-backed firms grant employee stock options can be explained by proxies for these economic and legal costs, and find that they can.

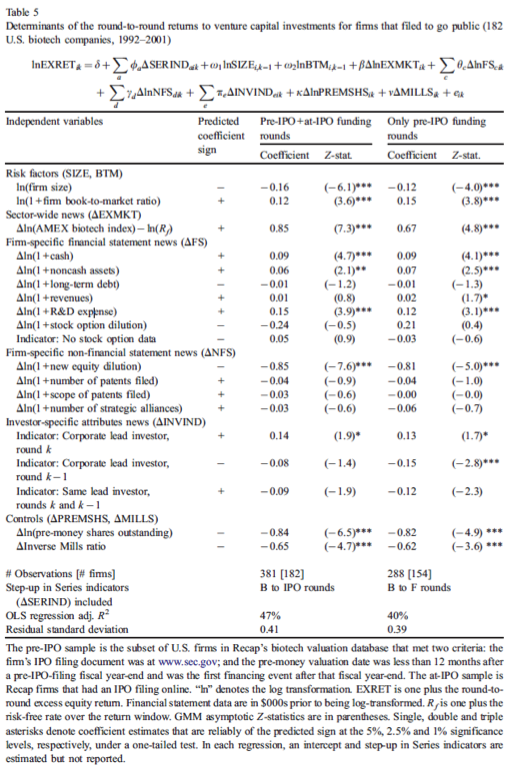

Determinants of the Round-to-Round Returns to pre-IPO VC Investments in U.S. Biotechnology Firms

Journal of Business Venturing (2007).

I propose that pre-IPO venture-backed biotech companies offer a useful and non-data snooped setting thru which to evaluate the relative merits of theories for why firm size and book-to- market explain variation in stock returns. This is because pre-IPO biotech firms have large and rapidly evolving growth options relative to assets-in-place, and such attributes align closely with the key features of Berk et al.’s (JF, 1999) model of the endogenous relations between growth options, optimal investment actions and expected equity returns. Using VC investments in pre-IPO U.S. biotech companies in 1992–2001, I find that equity returns between financing rounds are reliably negatively related to firm size and positively related to book-to-market ratios.